Business Ownership Coach | Investor Financing Podcast is about one simple idea: buy a business that pays you every month, not one that needs to be resold every month. If you want predictable cash flow, easier financing, and an exit that actually returns value, you need to think differently about franchise models. As a Business Ownership Coach | Investor Financing Podcast guide, this article breaks down five franchise types that deliver sticky, recurring revenue lenders love and buyers pay up for.

Why recurring revenue matters

There are two kinds of businesses. One sells once and hopes customers come back. The other sells once and gets paid every month. Banks, SBA lenders, and investors consistently favor the second type because recurring revenue is predictable. Predictability reduces churn, improves valuations, and makes financing and exits simpler.

Recurring revenue is not a nice-to-have — it is bankable. Contracts, subscriptions, auto-renewals, commercial accounts; these features turn cash flow from noisy and fragile into reliable and underwritable.

Model 1: Commercial cleaning (contract-based revenue)

Photo by Morgan Housel on Unsplash

Commercial cleaning franchises are commonly misunderstood as “janitorial” businesses. In reality they are contract plays. Offices, medical buildings, schools, gyms, and warehouses sign weekly or monthly cleaning contracts. Once you’re in, switching vendors is a hassle for facilities managers — which makes these accounts sticky.

- Revenue structure: weekly/bi-weekly/monthly recurring billing, auto renewals.

- Operations: semi-absentee ownership is possible — managers and subcontractors handle fulfillment while owners focus on sales and relationships.

- Finance and exit benefits: SBA friendly, easy to underwrite, low churn, scalable by adding accounts.

For buyers who want monthly predictability without reinventing acquisition every month, commercial cleaning is recurring revenue 101.

Model 2: Pest control (route density and retention)

Pest control might sound niche, but its business mechanics are powerful. The service sells prevention and peace of mind, and customers sign up for quarterly, monthly, or annual plans. People don’t cancel unless they move. Commercial clients like restaurants, apartment complexes, and warehouses nearly always maintain their plans.

- Why it sticks: fear-based need, regulatory pressure, habitual service schedules.

- Investor appeal: high route density, long customer lifetime value, strong resale multiples.

- Lender appeal: predictable cash flow, transferable accounts, low acquisition risk once routes are established.

Pest control is one of the more recession-resistant franchise models because the problem it solves is never optional when it affects health and operations.

Model 3: Modern laundromats (subscriptions plus real estate play)

Laundromats have been underestimated. Done right, they turn repeat behavior into weekly recurring customers. The modern formula layers traditional coin-op revenue with wash-and-fold subscriptions, pickup and delivery, and commercial accounts (Airbnb, gyms, salons).

- Recurring hooks: weekly usage, subscriptions for wash-and-fold or pickup/delivery, recurring commercial billing.

- Upside: combining business operations with real estate adds property appreciation, loan paydown, and tax advantages.

- Scale: add locations, offer new service tiers, or bundle with local delivery networks.

The laundromat model shines when you stop thinking in quarters and start thinking in habitual, recurring human behavior.

Model 4: Restoration and mitigation (insurance infrastructure)

Restoration and mitigation (water damage, mold, fire recovery, packouts) operate as insurance infrastructure. These businesses are not marketing-first; they are vendor-list businesses. Once approved by an adjuster, you get referred repeatedly. Recurring revenue in this sector often comes from repeating relationships and preferred vendor status rather than subscription billing.

- Revenue profile: high-ticket jobs, emergency services, frequent referrals from insurance adjusters.

- Why lenders and investors like it: fragmented industry with roll-up potential, predictable referral pipelines, fast scale by adding trucks and crews.

- Owner playbook: focus on relationship building with agencies and adjusters; scale location by location.

This model produces big checks and fast scaling opportunities because emergencies keep happening and insurance ensures payment flow.

Model 5: Medical and healthcare staffing (contracts on steroids)

Healthcare staffing is booming because the industry has a structural, long-term staffing shortage. Hospitals, clinics, and long-term care facilities need reliable staffing partners. Contracts often result in weekly billing, automatic renewals, and long client lifetimes.

- Stickiness drivers: chronic shortages, high switching costs, operational reliance on consistent staffing.

- Financial benefits: strong margins, asset-light model, recurring invoices that are easy to underwrite.

- Owner advantages: highly scalable regionally and executive-friendly to run.

Think of medical staffing as recurring revenue on steroids: predictable invoices, durable demand, and the ability to grow quickly through regional expansion.

Who these models are really for

These franchise models are not for everyone. They suit buyers who want predictable income, less volatility, and real asset value. High-earning W2 professionals, doctors, executives, and investors often gravitate to these options because they can transition from a paycheck to ownership without trading one form of work for another.

As a Business Ownership Coach | Investor Financing Podcast advisor, I often recommend starting with the business model rather than the brand. The right franchise model creates momentum: easier SBA approvals, higher valuations, and more desirable exits.

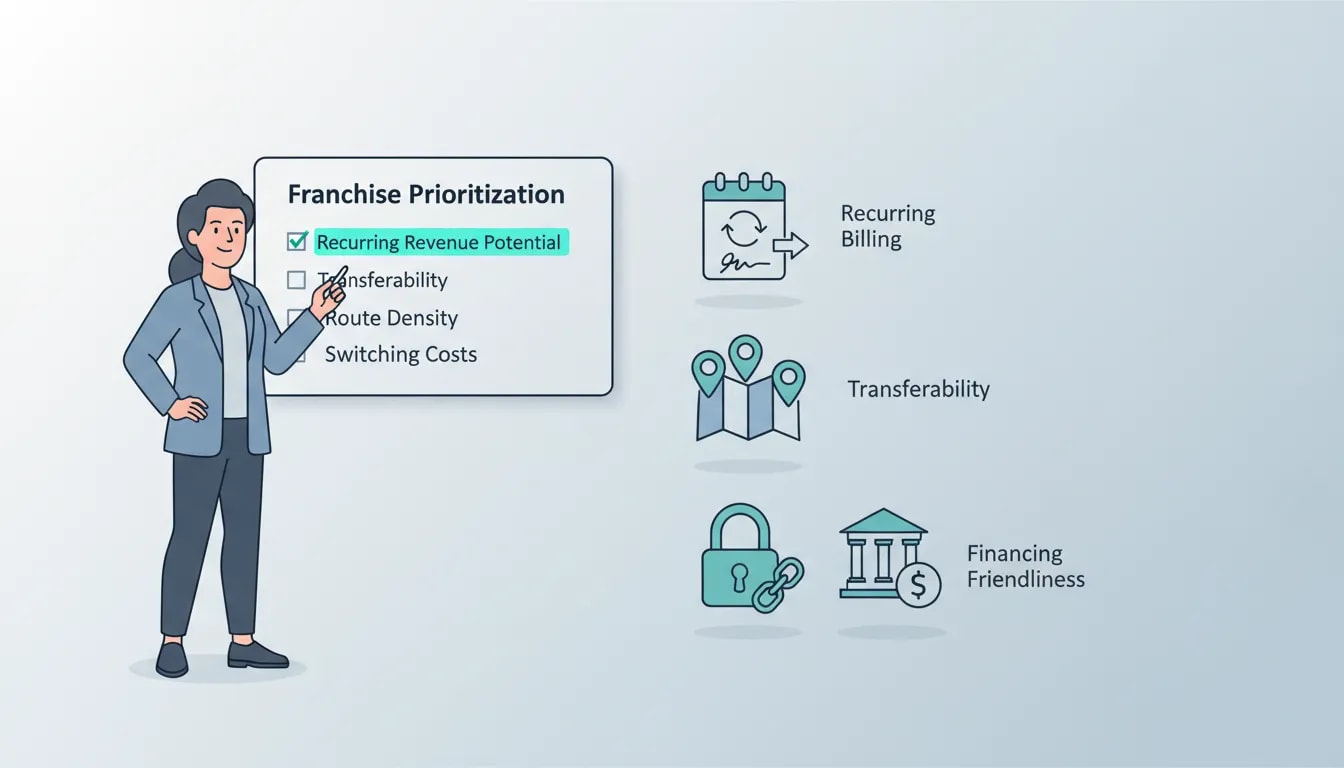

How to choose and what to prioritize

When evaluating opportunities, prioritize these criteria:

- Recurring billing mechanics: Are customers billed automatically on a regular basis?

- Contract length and transferability: Do accounts transfer at sale and are contracts multi-period?

- Route or account density: Can you cluster service calls to reduce marginal cost?

- Customer switching costs: How painful is it for a client to change providers?

- Financing friendliness: Will SBA lenders easily underwrite the cash flow and contracts?

Put another way: buy a system with invoices that repeat without you running an ad. That single change flips a business from “marketing dependent” to “finance friendly.”

Final takeaway

Owning the right business is the holy grail. The goal is not to work harder — it is to own a franchise that generates monthly, predictable revenue. If you want an asset that lenders like, buyers overpay for, and that pays you every month, start by choosing a model built around recurring cash flow.

If you want personalized guidance from a Business Ownership Coach | Investor Financing Podcast perspective, evaluate your capital, timeline, and appetite for operations, then match that profile to one of these five models. The right match changes everything.