Most people think paying taxes is mostly about “how much money you make” and “how smart you are.” Tom Wright, CPA, flips that assumption on its head. The tax code is not just a bill. It is a game with rules. And if you learn those rules, you can legally keep more of what you earn.

If you are a business owner, or you want to become one, this framework will feel empowering. The goal is not “gaming the system.” The goal is understanding how deductions work, how incentives work, and why tax results change when your income comes from a business rather than a paycheck.

Equity vs. Equality: Why the Same Outcome Depends on How You Operate

Here is the simplest way to understand the mindset shift. Equality means everyone does the same thing gets the same result. Equity means outcomes adjust based on effort, structure, and actions.

In taxation, the system does not reward “trying your best.” It rewards doing the right things the right way. Two business owners can start with similar situations, yet one may end up with a much higher tax burden than the other because their structures, strategies, and documentation are different.

That is why some small business owners can appear to pay very different amounts. One might be playing by the rules that create tax benefits. Another might be leaving deductions on the table or not qualifying for them at all.

Photo by Microsoft Copilot on Unsplash

Why Some Small Business Owners Pay 60% (and Others Pay Zero)

Tax outcomes vary because taxes follow categories and structures. If you are set up like an employee, you tend to get employee treatment. If you operate like a business owner, you can qualify for business treatment.

In practice, the difference often comes down to two things:

- Positioning your income correctly. Are you earning wages, or are you earning business income?

- Using the right strategies through the right professionals. Most people do not need more “tax tips.” They need the right tax advisor who understands how to structure plans so your deductions and investments actually qualify.

There is also a human factor. Some business owners invest in better teams, better operations, and better systems, and that can affect profitability and taxable income. But the tax side still requires intentional strategy.

Photo by Cosmin Serban on Unsplash

You Need a Good Tax Advisor, Not Just General Advice

One theme repeated throughout the discussion is that tax strategy is not a DIY hobby for most people. If you do not know what rules apply, you either miss benefits or accidentally infer “rules that are not there.”

That is where good advisors make a real difference. Wright’s CPA mission centers on helping mission-driven entrepreneurs and expanding their reach. The underlying logic is simple: when the goal is serving others, long-term wealth becomes a byproduct of doing the work, building the business, and structuring taxes correctly.

For many entrepreneurs, the fastest path to competence is learning from people who have already been through the battlefield. Wright and Beau Eckstein both emphasize financial education and learning from experienced authors and experts.

Tax as a Game: Learn the Rules Before You Guess

Taxes work with a basic principle: all income is taxable unless the law says it is not, and nothing is deductible unless the law says it is.

Once you internalize that, it becomes easier to stop chasing random “loopholes” and start asking better questions:

- What types of transactions create deductions?

- What qualifies as business expense versus personal spending?

- What tax incentives apply to the assets I am buying?

- How does my entity and classification affect my personal taxes?

This is why tax strategy is less about cleverness and more about precision.

Photo by Cosmin Serban on Unsplash

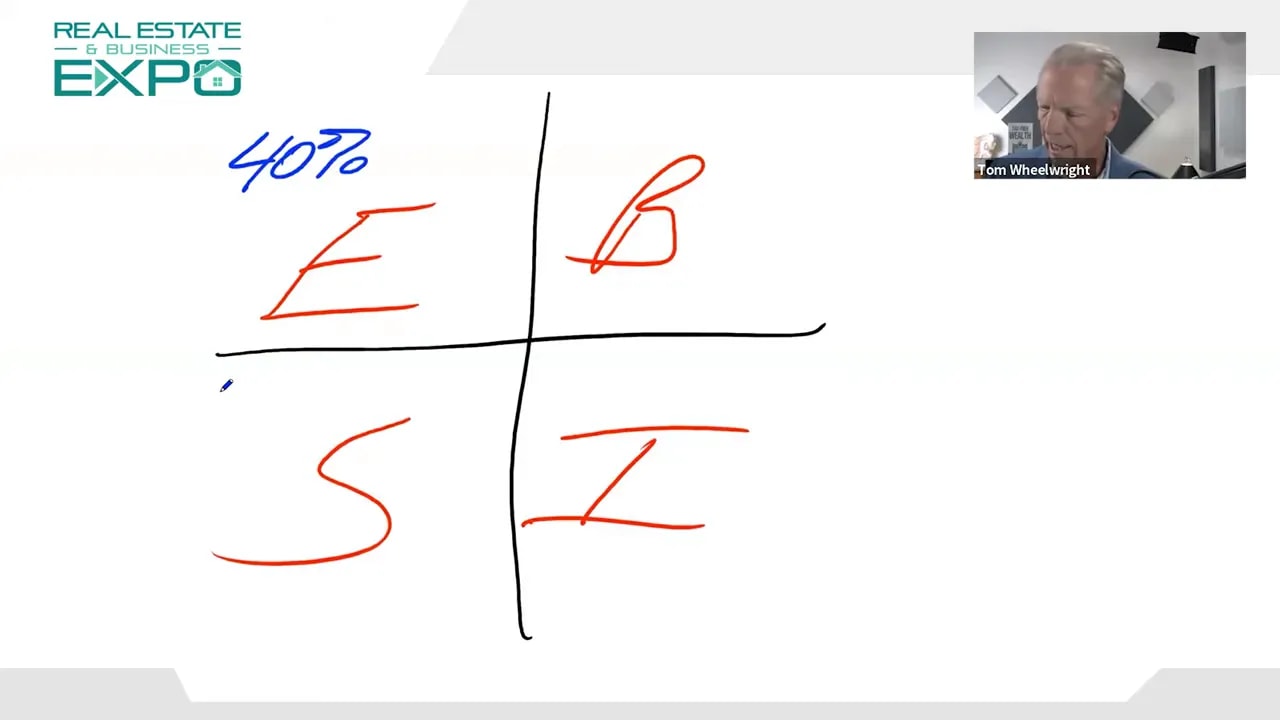

Robert Kiyosaki’s Cashflow Quadrant: Income Source Changes Your Tax Rate

Wright explains the core idea using the Cashflow Quadrant lens. There are essentially four ways people make money:

- Employee income (wages)

- Small business income

- Big business income

- Investor income (real assets aligned with government incentives)

The big takeaway is not that one category is “good” and another is “bad.” The takeaway is that how you make your money influences how you are taxed.

Wright’s rough illustration goes like this:

- As an employee, you may pay a higher effective rate.

- As you move toward business ownership, the tax rate can change.

- With professional investor strategies, it can be reduced dramatically.

- And when you combine business ownership with investor strategies, the system can produce outcomes that feel shocking compared to wage-based income.

This is also why Warren Buffett famously said he pays less tax than his secretary. The point is not about the person. It is about category and structure.

The #1 Tax Break: Why Business Ownership Often Wins

Wright makes a direct argument: the number one tax break in many situations is being a business owner.

Consider something most people did during COVID: working from home. An employee might not get meaningful deductions for that home office. A business owner can often deduct home office expenses when requirements are met.

The “why” matters. Tax law is fundamentally built on incentives. Governments want certain behaviors, such as:

- Jobs created and economic activity

- Technology created and business growth

- Food, housing, and energy investments

So the system favors structures that support those goals. That is how you get tax outcomes that seem lopsided when you compare wage earners to properly structured business owners.

Photo by Cosmin Serban on Unsplash

Equal Protection Under Law: You Do Not Have to Be Big to Get Big Results

One of the most encouraging parts of the discussion is the “equal protection” concept. Under the constitution, people doing the same things the same way should receive the same legal results.

Translated into practical strategy: you do not need to be a massive company to obtain tax results similar to larger businesses or investors. You need to do it the right way.

Small businesses create jobs, which can provide benefits. But the bigger opportunity comes when you do more than operate a business. You also invest strategically with assets that qualify for incentives.

First Ask: How Do You Make Your Money?

Wright emphasizes a two-part question that most people skip:

- How do you make your money?

- What do you do with the money you make?

The tax rate depends heavily on the first question. The second question determines which investments and strategies can reduce or eliminate taxable income.

He also points out that it is possible for very wealthy individuals to report surprisingly low taxable income when investments and expenses are structured properly. Again, the lesson is not gossip. The lesson is mechanics. Real assets, depreciation, leverage, entity classification, and incentives can dramatically change taxable outcomes.

Tax-Efficient vs. Tax-Effective Investments

Wright distinguishes between investments that are tax-efficient and those that are tax-effective.

- Tax-efficient often means the tax treatment is favorable for growth, such as Roth-style logic. You may not get immediate deductions, but the long-term tax result is better.

- Tax-effective means the investment can create deductions or other tax benefits that reduce taxable income.

Examples of investments aligned with government incentives include housing, energy, and food. The key is that you are not only investing for return. You are investing in a way that creates tax deductions through allowable rules.

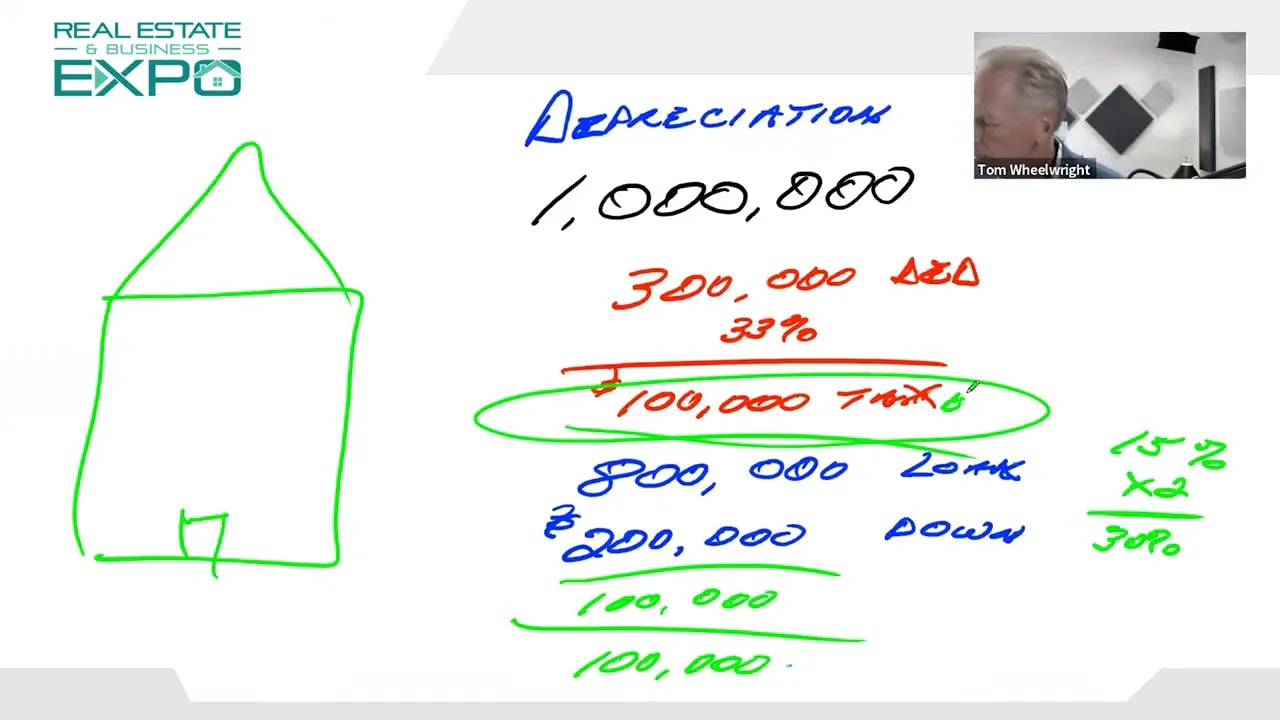

Real Estate Example: Bonus Depreciation and Cost Segregation

This is where the conversation gets very practical. Wright walks through a common real estate strategy: depreciation and bonus depreciation often used with cost segregation.

Start with a basic question many investors ask: “If I buy a rental property, shouldn’t I pay tax on the net income?”

Wright’s answer is: not necessarily, if you do it right. When properly structured, rental property deductions can reduce taxable income. One of those powerful deductions is depreciation, which is essentially the tax recognition of wear and tear on the property.

Here is the illustrative example:

- Assume a property cost of $1,000,000.

- With strategies like cost segregation, you might get around $300,000 in bonus depreciation (numbers vary by facts and rules).

- If you are in a 33% combined federal and state bracket, that could equate to about $100,000 of tax benefit.

- But the real wealth-building effect comes from leveraging the investment. If you use financing, your down payment is smaller, and the tax benefit can increase your effective return.

Wright frames it as compounding. Tax benefits plus equity growth can create a powerful “double win”: increasing net worth while reducing taxes.

Double Wins: Increasing Net Worth While Reducing Taxes

Many people view taxes only as a cost. The more useful mindset is viewing taxes as something that can be managed through structure and investment decisions.

With the right approach, deductions do not just lower your tax bill. They can also make real estate returns more attractive, since you are improving your after-tax outcome. That is how strategies shift from “saving a little” to building wealth.

Offset W2 Income With the Right Entity Setup (When Eligible)

Another practical point is that some strategies can potentially offset wages too, depending on how your situation is structured.

Wright and Beau discuss that business owners who have both W2 income and qualifying real estate deductions may be able to offset some of that W2 income. In many cases, a large portion of wages can be reduced, within IRS limitations and based on eligibility.

The key word here is potentially. This depends on facts, entity structure, and qualification rules. That is why working with a CPA or tax advisor who understands these strategies matters.

Why Mission-Driven Entrepreneurs Build Better Wealth

Wright’s mission statement is not just marketing. It reflects the approach: serve mission-driven entrepreneurs and help expand their reach.

When you combine that mindset with education, it changes the decision-making process. You stop thinking like a person trying to avoid taxes and start thinking like a builder who wants to create jobs, deliver value, and reinvest into assets that align with incentives.

Franchises Can Be a Faster Path to Ownership (With Systems Already Built)

Beau and Wright also touch on franchising. The advantage is that you are not starting from scratch. Systems, marketing, and operations are often already packaged, which can help business owners grow faster.

And from a tax and ownership perspective, the more important idea is the same: business ownership is often the foundation for tax advantages. If franchising is a practical route to ownership for you, it may reduce the time and complexity required to get there.

Action Steps to Stop Overpaying Taxes (Legally)

- Get clear on your income category. Are you earning wages, business income, or investor income?

- Confirm deductions you qualify for. Don’t assume. Validate with documentation and rules.

- Build a strategy that includes real assets. Housing, energy, and food aligned investments can create tax-effective outcomes.

- Ask about depreciation and cost segregation for real estate. This is often where the math turns.

- Use a tax advisor who thinks in structures, not tips.

Bottom Line: Learn the Rules, Build the Business, Invest With Incentives

Stop overpaying taxes by doing something more powerful than “trying harder.” Learn the rules, structure your ownership correctly, and invest in ways that qualify for legal incentives.

Business ownership is not just a career choice. It can be a wealth-building engine because it changes how the tax system treats your income and deductions.

Business Ownership Coach | Investor Financing Podcast: keep building smarter systems, stay mission-focused, and use legal tax strategies to compound wealth over time.

Need Financing to Build the Business?

If you’re working through entity setup, deductions, and real-asset strategies, the next question is often funding. If you’re considering SBA loan options for business acquisition, franchise startup, working capital, or refinancing, you can check your eligibility here: SBA loans.

Use the form to share your basic financial snapshot so lenders can better assess your fit and next steps—then pair that financing plan with the tax strategy framework from this article.